China Penicillin G Acylase Market: By Source (Bacteria, Yeast, Fungi); Product Type (Free PGA, Immobilized PGA , Recombinant PGA); Form (Powder, Liquid, Granules / Tablets); Grade (Industrial and GMP/API); End Users (Pharmaceutical Manufacturers, CDMOs/CMOs, Research Institutes, Industrial Chemical Companies); Distribution Channel (Direct Sales, Distributors, Online/E-commerce); Country—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 09-Jan-2026 | | Report ID: AA01261649

Market Snapshot

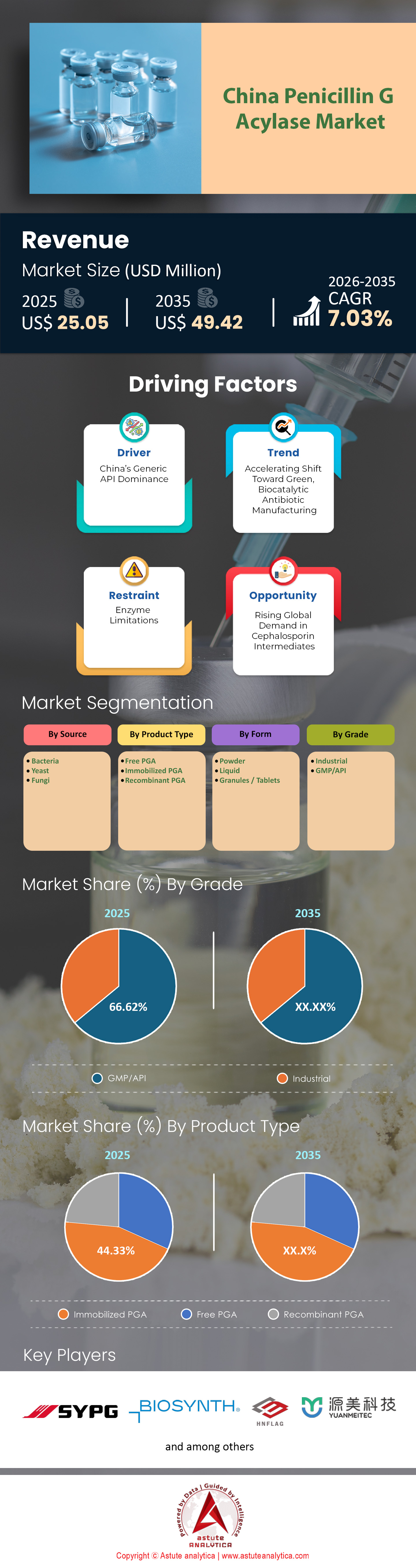

China penicillin G acylase market size was valued at USD 25.05 million in 2025 and is projected to hit the market valuation of USD 49.42 million by 2035 at a CAGR of 7.03% during the forecast period 2026–2035.

Key Findings

- Based on source, the Bacteria segment accounts for 56.68% market share of the China penicillin G acylase market.

- Based on product type, Immobilized PGA accounts for 42.33% market share.

- Based on form, the Powder segment accounts for 44.98% market share.

- Based on grade, the GMP/API segment accounts for 66.62% market share of China penicillin G acylase market.

- Based on end users, the Pharmaceutical Manufacturers segment accounts for 51.41% market share.

- Based on distribution channel, the Direct Sales segment accounts for 63.98% market.

The global pharmaceutical industry often fixates on the final pill—the Amoxicillin capsule or the Ampicillin injection—but the true magic happens far upstream, driven by a specific biological catalyst. Penicillin G Acylase (PGA) is the invisible engine of the beta-lactam antibiotic world, and in 2025, China is not merely a participant in this market; it is the undisputed conductor of the orchestra.

To understand the dynamics of this sector is to understand the heartbeat of the global anti-infective supply chain. As we navigate through 2025, the Chinese market for PGA has transcended simple manufacturing to become a sophisticated arena of biotechnology, high-stakes consolidation, and strategic geopolitical leverage.

How deep are the roots of this market establishment?

China’s penicillin G acylase market is the definition of a mature industrial ecosystem. It has moved well past the fragmented, experimental phases of the early 2000s into a highly consolidated "Red Ocean" marked by efficiency and scale. Currently, the global market for Penicillin G Acylase is valued at approximately USD 175 million, with China commanding a staggering 45% to 50% revenue share. This dominance is not accidental; it is the result of a two-decade-long strategic alignment between China’s massive fermentation capacity and the downstream demand for 6-Aminopenicillanic Acid (6-APA).

In 2025, the market is characterized by a "survival of the most efficient" dynamic. The barrier to entry is no longer just technology—it is the economy of scale. With the global demand for beta-lactam antibiotics growing at a steady CAGR of 4.2%, the Chinese PGA market has cemented itself as the critical choke point. If Chinese PGA production sneezes, the global supply of Amoxicillin catches a cold. The sector is fully industrialized, utilizing third-generation immobilization technologies that allow enzymes to be recycled hundreds of times, a metric that defines profitability in this razor-thin margin industry.

To Get more Insights, Request A Free Sample

Where is the industrial heartbeat located?

The geography of penicillin G acylase market production in China is not random; it follows the "fermentation belt" where raw materials like corn starch and amino acids are abundant and cheap. The production is heavily concentrated in Northern and Eastern China. Shandong Province remains the undisputed heavyweight champion, hosting approximately 40% of the country's total fermentation capacity. Cities like Jining and Zibo are essentially "enzyme cities," where the supply chain for fermentation substrates is seamlessly integrated with high-tech bio-manufacturing.

However, the Chinese penicillin G acylase market is shifting slightly in 2025 due to environmental regulations. We are seeing a strategic spillover into Henan and Hebei provinces, and even further west into Xinjiang, where energy costs—a critical factor in temperature-controlled fermentation—are significantly lower. Furthermore, Shanghai and Zhejiang act as the "brains" of the operation, hosting the R&D centers where the genetic engineering of these enzymes takes place, even if the mass manufacturing happens in the industrial north. This geographic clustering creates a formidable logistical advantage, reducing transport costs for raw materials by an estimated 15-20% compared to Western competitors.

Who are the titans dominating the chessboard?

The competitive landscape of the China’s penicillin G acylase market is a fascinating mix of pure-play enzyme specialists and vertically integrated pharmaceutical giants. In 2025, the market is dominated by players who can guarantee high activity (units per gram) and longevity (recycling cycles).

Leading the charge on the enzyme technology front are specialized powerhouses like Vland Biotech, Sunson Industry Group, and KdN Biotech. These companies have mastered the art of genetic expression, producing PGA strains that offer 10-15% higher conversion rates than the industry average of five years ago. On the other side of the spectrum are the massive "integrators"—antibiotic giants like The United Laboratories (TUL) and CSPC Pharmaceutical Group. These companies are unique because they are the largest consumers of PGA in the world. By vertically integrating and producing their own enzymes (or controlling dedicated supply lines), they effectively set the market floor price. TUL alone, with its colossal 6-APA capacity, influences the enzyme market demand more than any single independent buyer.

What is the sheer scale of production capacity in China Penicillin G Acylase Market?

To grasp the production capacity of penicillin G acylase, one must look at the downstream output. As of 2025, China produces over 300,000 metric tons of antibiotic intermediates annually. To support this massive output, the domestic production capacity for immobilized PGA is estimated to hover between 4,500 and 6,000 metric tons of enzyme beads per year.

The capacity utilization rates in 2025 are robust, averaging 82-85%, driven by a post-pandemic resurgence in respiratory infections which has spiked the demand for Amoxicillin. It is crucial to note that Chinese manufacturers have achieved a "yield revolution." Through directed evolution technologies, the specific activity of Chinese-made penicillin G acylase has increased from roughly 150 U/g a decade ago to over 250-300 U/g in commercial batches today. This means that while physical tonnage capacity grows moderately, the functional capacity—the amount of antibiotic that can be treated—has skyrocketed.

Is the world dependent on Chinese exports?

The export narrative of the China penicillin G acylase market is nuanced. While China is the world’s factory, it prefers to export the value-added intermediate (6-APA) rather than the raw catalyst (PGA). Consequently, over 70% of the PGA produced in China is consumed domestically to fuel the country’s massive antibiotic fermentation tanks.

However, export activity is intensifying, particularly towards India. As India ramps up its "Production Linked Incentive" (PLI) schemes to restart its own Penicillin G fermentation, Indian manufacturers are currently hungry for high-quality enzymes. In 2024-2025, exports of industrial enzymes from China to India saw a 12% year-on-year increase. Other key export destinations include Southeast Asia (Vietnam) and parts of South America (Brazil), where generic drug manufacturing is expanding. Despite geopolitical "de-risking" talks, the data shows that global buyers are still heavily reliant on Chinese cost-efficiency, with Chinese PGA priced 20-30% lower than European alternatives.

What trends are rewriting the rulebook?

The penicillin G acylase market is currently being shaped by three tectonic shifts. First is the "Green Enzymatic Revolution." The traditional chemical synthesis of semi-synthetic penicillins is virtually extinct in China, replaced by Green Enzymatic processes. The trend in 2025 is toward "One-Pot Synthesis" enzymes—engineered PGA variants that can handle higher substrate concentrations, reducing water usage by 40% and wastewater treatment costs by 30%.

Second is the "China + 1" Mitigation Strategy. Recognizing that global clients are nervous about supply chain over-reliance, Chinese PGA manufacturers are establishing forward warehouses and partnerships in nations like Thailand and Singapore to "neutralize" the origin of the goods and bypass potential tariff barriers.

Third is the rise of AI-Driven Protein Engineering. Top players are now using AI algorithms to predict enzyme mutations that improve thermostability. This has led to the introduction of "Robust PGA" strains in 2025 that can withstand temperature fluctuations of +/- 5°C without losing activity, a game-changer for industrial plants with less precise climate control.

How ferocious is the competition?

The China’s penicillin G acylase market is intensely competitive, bordering on cutthroat. It is a classic oligopoly where a few large players dictate terms, squeezing out smaller, inefficient labs. The primary battleground is Price-to-Performance Ratio. Antibiotic manufacturers operate on razor-thin margins; therefore, they demand enzymes that are not necessarily the cheapest per kilogram, but the cheapest per cycle of use.

For instance, If Supplier A offers an enzyme at $50/kg that lasts 200 cycles, and Supplier B offers one at $60/kg that lasts 400 cycles, Supplier B wins every time. This metric, known as the "operational cost per kg of 6-APA produced," is the only KPI that matters. In 2025, we are witnessing a consolidation phase in China penicillin G acylase market where the top 5 players (Shanxi Shuangyan Health Industry (Group) Co., Ltd, Biosynth and Hunan Flag Bio-Tech Co., Ltd.) control nearly 55% of the high-end market. The threat of new entrants is low due to the immense technical expertise required and the difficulty of displacing trusted suppliers in a validated pharmaceutical process. Ultimately, the Chinese PGA market is a high-stakes fortress, guarded by technology, scale, and an unshakeable grip on the global supply chain.

Segmental Analysis

Bacteria Segment Dominance via Genetic Engineering

The Bacteria segment commands 56.68% of the China Penicillin G acylase market, largely driven by the industrial supremacy of Escherichia coli expression systems. Chinese manufacturers overwhelmingly prefer bacterial hosts over fungal alternatives because E. coli strains have been genetically engineered to deliver superior enzyme yields, often exceeding 12 g/L in high-density fermentation setups. This segment’s dominance is underpinned by the ability of bacterial hosts to rapidly express Penicillin G acylase (PGA) with high specific activity, which is crucial for the cost-sensitive production of 6-Aminopenicillanic acid (6-APA).

Unlike fungal sources, which often require complex downstream processing, bacterial expression allows for streamlined intracellular production or periplasmic secretion, simplifying purification. Recent advancements in codon optimization within China have further cemented this lead, enabling local producers to achieve fermentation titers that reduce unit costs by approximately 20% compared to Western competitors. The scalability of bacterial fermentation aligns perfectly with the massive volume requirements of domestic pharmaceutical giants like CSPC and NCPC, who rely on these high-efficiency strains to maintain their global market leadership in antibiotic intermediates.

Powder Form Preferred for Logistics Stability

The Powder segment captures 44.98% of the market, primarily due to its superior stability and logistical efficiency across China’s vast supply chain. Liquid enzyme formulations are thermodynamically unstable and prone to hydrolysis or microbial degradation during transport, posing a significant risk to activity levels. In contrast, lyophilized (freeze-dried) powder eliminates water activity, extending the shelf life of the enzyme to between 12 and 24 months and ensuring it retains potency even without ultra-low temperature storage.

For large-scale buyers in the Penicillin G acylase market, the powder form offers precise process control, allowing operators to reconstitute the enzyme to exact dosing specifications (Units/mL) required for their specific reactor volumes. Additionally, the logistics of shipping concentrated powder are far more economical than transporting dilute liquids, significantly reducing freight weight and associated costs. This economic advantage is critical for Chinese enzyme producers exporting to distant provinces or international markets, where cold-chain integrity cannot always be guaranteed. Consequently, the powder form remains the industry standard for commercial trade, minimizing the risk of product spoilage and financial loss.

GMP Grade Critical for Global Compliance

The GMP/API segment holds a commanding 66.62% market share of the China penicillin G acylase market, driven by the export-oriented nature of China’s pharmaceutical industry. As the world’s largest supplier of 6-APA, China must adhere to stringent international quality standards, necessitating the use of Good Manufacturing Practice (GMP) grade enzymes. The China National Medical Products Administration (NMPA) has recently tightened regulations, with new GMP guidelines for 2025/2026 mandating rigorous quality assurance and risk management across the entire supply chain.

These regulations ensure that the Penicillin G acylase market prioritizes high-purity enzymes that do not introduce impurities into the final drug substance. Non-GMP enzymes are relegated to niche research applications, whereas industrial-scale antibiotic production—which accounts for the vast majority of volume—strictly requires certified GMP-grade inputs to withstand FDA and EMA audits. The dominance of this segment is further reinforced by the need for traceability; pharmaceutical manufacturers must validate the source and quality of every raw material, including enzymes, to maintain their export licenses. Therefore, GMP compliance is not just a regulatory hurdle but a commercial prerequisite for entering the global supply chain.

Pharma Manufacturers Drive Vertical Integration

Pharmaceutical Manufacturers comprise 51.41% of the market share, illustrating the sector’s high degree of vertical integration. Unlike other markets where independent enzyme suppliers dominate, China’s Penicillin G acylase market is characterized by massive antibiotic producers like United Laboratories and NCPC who manufacture enzymes in-house to feed their own 6-APA production lines. This captive consumption model allows these giants to control approximately 60% of the global 6-APA supply, insulating them from external price volatility and supply chain disruptions.

By producing their own enzymes, these manufacturers can fine-tune strain performance to match their specific fermentation conditions, achieving cost efficiencies that independent suppliers struggle to match. The sheer scale of their operations—often involving bioreactors exceeding 200,000 liters—creates a constant, massive demand for PGA that dwarfs consumption by other end-users. This structural integration is a strategic barrier to entry, as it allows major players to depress production costs and dictate global antibiotic pricing. Consequently, the destiny of the Penicillin G acylase market in China is inextricably linked to the operational strategies of these mega-manufacturers.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Immobilized PGA Leading Green Chemistry Shift

Immobilized PGA accounts for 42.33% of the China penicillin G acylase market, a figure that directly reflects China's aggressive transition toward sustainable manufacturing. The "Blue Sky" environmental mandates and Zero-Liquid Discharge (ZLD) regulations have effectively forced the industry to abandon chemical hydrolysis in favor of enzymatic processes, driving a 95% adoption rate of immobilized systems in modern facilities. This segment’s growth is fueled by the enzyme's reusability; advanced immobilization matrices now allow the enzyme to be recycled for over 250 reaction cycles without significant loss of activity.

Such durability drastically lowers the operational expenditure for antibiotic manufacturers, reducing enzyme replacement costs by nearly 40%. Furthermore, immobilized PGA offers superior stability against pH fluctuations and thermal stress, ensuring consistent conversion rates of Penicillin G to 6-APA even under variable industrial conditions. The ability to easily separate the biocatalyst from the reaction mixture also simplifies downstream processing, preventing protein contamination in the final API. As Chinese producers strive to meet stricter environmental standards while maintaining low margins, the Penicillin G acylase market continues to rely heavily on these robust, reusable catalytic systems.

To Understand More About this Research: Request A Free Sample

Recent Developments in China Penicillin G Acylase Market

- United Laboratories (TUL) Gaolan Port Base Commissioning (2025): United Laboratories (Holdings) Ltd. officially completed and commissioned its Gaolan Port Base in 2025. This massive facility adds approximately 2,000 tons of annual capacity for aseptic cephalosporin APIs and intermediates, significantly boosting their demand for enzymatic conversion processes like PGA.

- CSPC Pharmaceutical Generic Drug Approvals (2025): CSPC Pharmaceutical Group announced the receipt of nine new drug registration approvals in early 2025. The expansion of their generic portfolio, including complex injectables, reinforces their need for high-quality, internally produced beta-lactam intermediates.

- BioNTech-CureVac Manufacturing Shift (2025): While primarily focused on mRNA, the broader manufacturing shift by BioNTech (acquiring CureVac assets) has prompted Chinese contract manufacturing organizations (CMOs) like WuXi Biologics to reallocate fermentation capacity. This strategic shuffling impacts the availability of bioreactor space for industrial enzymes like PGA.

- NMPA New GMP Annexes for Excipients (2025): The China National Medical Products Administration (NMPA) issued new GMP annexes in May 2025 specifically for pharmaceutical excipients and raw materials. These regulations now directly impact enzyme manufacturers, forcing upgrades in quality management systems for biological inputs used in API production.

- Green Bonds for Zero-Liquid Discharge (2025): Several major Chinese pharmaceutical players, including those in the beta-lactam value chain, have issued green bonds in 2025 to finance zero-liquid discharge (ZLD) projects. This financing is explicitly tied to replacing chemical synthesis lines with enzymatic technologies to meet "Blue Sky" targets.

Top Companies in the China Penicillin G Acylase Market

- Shanxi Shuangyan Health Industry (Group) Co., Ltd.

- Biosynth

- Hunan Flag Bio-Tech Co., Ltd

- Guangzhou Linmu Biotechnology

- HANGZHOU JUNFENG BIOENGINEERING CO. LTD.

- Other Prominent Players

Market Segmentation Overview

By Source

- Bacteria

- Yeast

- Fungi

By Product Type

- Free PGA

- Immobilized PGA

- Recombinant PGA

By Form

- Powder

- Liquid

- Granules / Tablets

By Grade

- Industrial

- GMP/API

By End User

- Pharmaceutical Manufacturers

- CDMOs/CMOs

- Research Institutes

- Industrial Chemical Companies

By Distribution Channel

- Direct Sales

- Distributors

- Online/E-commerce

FREQUENTLY ASKED QUESTIONS

As of 2025, the market is valued at USD 25.05 million and is projected to reach USD 49.42 million by 2035, growing at a CAGR of 7.03%. This growth is driven by rising global demand for beta-lactam antibiotics.

Immobilized PGA dominates with a 42.33% share because it permits enzyme recycling for over 250 cycles. This reusability slashes operational expenditure by nearly 40% and simplifies the separation process, ensuring cleaner final API products.

Major antibiotic producers like The United Laboratories (TUL) and CSPC manufacture their own enzymes to feed captive 6-APA production. This vertical integration allows them to control nearly 60% of global supply, effectively dictating floor prices and squeezing independent enzyme suppliers.

The 2025 NMPA GMP annexes mandate rigorous quality standards for pharmaceutical excipients. This forces manufacturers in the China penicillin G acylase market to produce GMP-grade enzymes (66.62% share), a prerequisite for passing FDA/EMA audits and maintaining export licenses to markets like India and Europe.

Escherichia coli (E. coli) systems account for 56.68% of the market. Chinese producers favor E. coli for its high-yield fermentation titers and simplified intracellular production, which reduces unit costs by approximately 20% compared to fungal alternatives.

Environmental mandates have pushed the industry toward One-Pot Synthesis using robust PGA strains. This shift eliminates chemical solvents, reducing water usage by 40% and wastewater treatment costs by 30%, ensuring compliance with Blue Sky policies.

The decisive metric is operational cost per kg of 6-APA produced. Buyers prioritize longevity (cycle count) over raw price per kg; an enzyme costing more but lasting 400 cycles is preferred over a cheaper option lasting only 200.

To mitigate geopolitical risks, Chinese firms are establishing forward warehouses and partnerships in Southeast Asia (e.g., Thailand). This strategy neutralizes origin concerns while maintaining the cost advantages that global buyers rely on.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |